[ad_1]

in economics The components of a company’s operating costs are calculated and analyzed using various variables. It aims to generate comprehensive and effective analytical results for decision making.

The variables of cost analysis are total cost (total cost), average cost (average cost) Fixed and variable costs (fixed and variable costs) and incremental costs (incremental cost).

After calculating for a while The above variables can be described as curves. The intersections between the curves of the above variables show possible indirect decisions in the company.

in the following article The authors will discuss just one component of variable costs. which is incremental cost Check out the full review below:

Definition of Marginal Cost

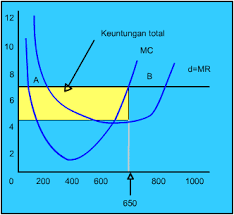

incremental cost (incremental cost) is the change in total cost of production due to an increase of 1 unit of output produced by the firm. In economic terms, quantity incremental cost The company may vary depending on the stage of business carried out by the company dot dot dot. incremental cost Over time, they can combine to form a so-called curve. marginal cost curve (incremental cost curve). This curve is initially concave as the company grows and eventually increases. This is an example image. incremental cost curve

At some point, the curve intersects with the average cost curve (average cost) and additional income (incremental income). One company’s production is said to be efficient if the curve incremental cost (MC) of the company intersects the curve. incremental income (M.R.W.) and average cost (January).

This can happen due to increased production volumes. total cost and incremental cost will increase. temporarily average cost issued by the company will decrease first and then increase.

In addition to AC and MR, analysis incremental cost It can also cover more if you combine it with curves. total cost and gross income (Tr). Since with these two additional curves You can know to what extent your company can optimize production.

marginal cost formula

The incremental cost formula is pretty simple, namely:

Marginal Cost = (Change in Cost) / (Change in Total Production Quantity)

or

Marginal cost = (TC2- TC 1) / (Q2 – Q1)

or

MC = ∆TC / ∆Q

in economic mathematics rules incremental cost It is often called the top derivative (derivative) of total cost or TC’.

You must keep in mind that marginal costs are different from average costs. average cost It is the average cost incurred by the company to produce one unit of output. for that recipe average cost is:

AC = TC/Q or the total cost of production divided by the total quantity of goods produced.

How to calculate incremental cost

There are only 3 steps to calculating incremental costs:

- Gather information about total cost and total output from two different times.

- Subtract the second and first total costs and the second and first total output.

- Divide the total cost reduction result above by the total output reduction result.

Example of incremental cost

Simple example:

P.T. ABC is a company that produces flower arrangements. In November and December 2022, the company spent IDR 5,000,000 and IDR 6,000,000 respectively for production costs. meanwhile The number of flower bouquets the company produces in November is 25 and in December 30. Therefore, incremental costis:

Marginal cost = (TC 2- TC1) / (total quantity 2 – total quantity 1)

Marginal cost = (6,000,000- 5,000,000) / (30 – 25)

= 1,000,000/5= 200,000.

tricky example

Here is a slightly convoluted example to help you distinguish between average cost (Bor Chor.) and incremental cost (M.C).

| g | b | c | D | e |

| month | Q (number of goods produced in a unit) | Total cost (TC) | incremental cost ((C4-C3)/(B4-B3) | Average cost (C3/B3) |

| 1 | 100 | 2,000 | 20 | |

| 2 | 200 | 2,300 | 3 | 11.5 |

| 3 | 300 | 2,400 | 1 | 8 |

| 4 | 400 | 2,525 | 1.25 a.m. | 6,3 |

| 5 | 500 | 2,775 | 2,5 | 5.55 a.m. |

| 6 | 600 | 3300 | 5,25 | 5,5 |

| 7 | 650 | 3520 | 4.4 | 5.415384615 |

| 8 | 700 | 4000 | 9,6 | 5.714285714 |

| 9 | 800 | 6,400 | 24 | 8 |

from the table above It can be seen clearly that MC and AC will almost intersect when the quantity produced reaches 600 units and the total cost incurred is 3300 in this example. It can be seen that the company can still increase the production volume to 650 units and the MC and AC values will decrease.

However, if the company continues to force production to 700 MC and AC will increase further. Therefore, it can be said that the increase in production does not correspond to the increase in costs.

The calculations in the table above get more complicated if you divide total costs into total fixed costs (fixed cost) and variables (variable value). This is because the total cost is the result of adding the two components together. And each cost component has different characteristics.

Marginal cost function

counting function incremental cost Is to determine the level of efficiency the company can operate. Efficiency here means that a company can produce a large number of products while still reducing production costs.

Is incremental costing also a very useful concept to help a pre-ordered company increase production? For example, the company currently has a plant with a production capacity of 650 units per day and a total cost of 3,520 units per day. It wouldn’t make sense if the company had agreed to order 50 more units if the total cost was capped at 4,000 units per day and the incremental cost had increased to 9.6 from the initial 4.4.

Conclusion

incremental cost (incremental cost) is a type of variable cost used to calculate the amount of change in total cost (TC) if one unit of output (q) is added. This theory is important in determining the level of production efficiency of a company.

[ad_2]

Source link

{kind=link}