[ad_1]

Assets and liabilities are two bookkeeping concepts that people and investors should understand. The layman needs to understand this concept to be able to better organize their personal and business finances. While investors need this concept to be able to properly read and analyze the company’s finances.

However, before you can understand the differences in the use of these two words. You should first understand the meaning of the following assets and liabilities:

definition of assets

Assets are resources that a company can use to make profits or fulfill future obligations. Another word that is often used to refer to property is property or property.

In financial statements, assets are arranged according to their liquidity from the easiest to trade or sell to the hardest to sell. Here’s the command:

- Cash/cash.

- cash equivalents These cash-equivalent assets are financial instruments that can be quickly disbursed in addition to cash, for example, savings or bank deposits, checks, savings accounts, and much more.

- trade accounts receivable

- Inventory (list of items).

- equipment such as consumables

- equipment such as machinery, laptops, computers

- building and

- Pre-paid fees. For example, you buy electricity by top-up or top-up before using electricity. This electricity charge will later be included in the prepaid electricity bill. And the value decreases as you consume electricity.

meaning of passive

Liabilities are obligations that a company must pay to third parties in the future. Broadly speaking, liabilities include debt, revenue, capital, and expenses to be paid. When detailing again, this section of the financial statements will consist of

- short-term debt (current liabilities)Including debts that must be paid within a period of not more than 1 year, including creditors expenses to be paid Bonds with a maturity of less than 1 year, and many more.

- long-term debt (long term debt)Including debt instruments with a maturity of more than 1 year such as bank debt or bonds with maturities over 1 year.

- unrealized income (deferred income). In accounting, if buyer make DP or pay your service in full. but you have not performed the service yet Money from the buyer must be recorded as deferred income. Since you have not fully performed your duties, therefore the customer can still withdraw the money.

Formula for Asset and Liabilities Balance Sheet

general formula

broadly The asset-liability relationship can be described by the following formula:

Assets = Liabilities (Liabilities) + Equity

Capital (shareholders’ equity) It is the amount deposited by the company’s founders and/or investors. If the amount of liabilities plus equity is not equal to assets There is something wrong with the financial records you are working on.. Because accountants have to enter transaction data into assets and liabilities simultaneously to record them in a general journal.

For example, a dormitory tenant puts a rental deposit for the next 3 months in the amount of IDR 1,200,000 when entered into the general journal. You must record cash (assets) deducted in the amount of IDR 1,200,000 and prepaid income (deferred income/ liability) in credit with the same amount. This aims to ensure that there are no errors when entering data.

For better financial analysis purposes Investors or financial analysts often perform more detailed calculations. Here are some of them:

current assets

Current assets result from the sum of assets that can be liquidated quite simply. The formula:

Current Assets = Cash + Cash Equivalent Assets* + Total Goods + Receivables + Marketable Securities + Prepaid Expenses + Other Liquid Assets

current liabilities

Current liabilities are all liabilities that must be repaid in the short term. The formula is:

Current Liabilities = Bills Payable + Trade Accounts Payable + Short-Term Loan + Accrued Expenses + Prepaid Income + Long-Term Debt*+ Other Short-Term Debt

information:

Promissory notes are short-term debts in the form of promissory notes.

Long-term debt* is part of long-term debt. For example, you owe the bank Rs. 10,000,000 in 2021 with at least 20% annual repayment and must be paid in full by 2025. So what is calculated above is not Rs.10,000,000, but to 20% * 10,000,000 to be paid in 2023

compare between current assets and current liabilities This is what is called current ratio. current ratio Demonstrates the company’s ability to pay off short-term debt. the higher the value current ratio, The financial position of the company will only improve.

fixed asset formula

Fixed assets = Total fixed assets – Accumulated depreciation

in addition current ratioThe asset and liability components are also used in the calculation of other financial ratios such as Debt to asset ratio (DAR) to compare liabilities (especially short-term) with assets or Cash Flow to Debt Ratio to compare the total cash and liabilities of the company.

These ratios are used by lenders and investors to determine the financial health of a company. Because a company with good financial status is a company that can fulfill its obligations (debts) both in the short term and in the long term.

Types of Assets and Liabilities

asset type

1. Current assets

Current assets, also known as current assets It is a type of asset that is liquid (liquidated) easily, so the value of the asset can change all the time. An example is cash. because the value changes rapidly Cash changes are therefore recorded in a separate report known as the cash flow statement.

2. Fixed assets

Fixed assets, often called fixed assets It is a type of asset that is quite difficult to liquidate. And the value of assets is not easy to change in one year, such as machinery, buildings, equipment, etc.

Although there is a change But it is usually only in the form of a concept where the value is recorded as depreciation. Depreciation is the cost incurred by reducing the useful value of an asset. This value appears because if used for a long time The value of fixed assets will decrease and can reach 0.

For example, you bought a graphics laptop worth Rp 10,000,000 with about 5 years of use, so the average depreciation of the notebook in each year is INR 2,000,000 and in the fifth year the notebook is no longer usable. or can be used but must be repaired several times

3. Tangible assets

Tangible assets are assets that can be seen and touched, such as machinery, cash, office equipment, etc.

4. Intangible assets

Intangible assets are assets that can be profitable in the future but cannot be touched. Examples include copyrights, franchise licenses, and so on. You must legally purchase a franchise license from the company. This license may not be touched or seen by anyone. but with this license You can easily run your transport business.

Licenses, copyrights or industrial property rights are invisible assets. But just like fixed assets. Usually reduced in value, for example, if you want to open a cooperation with a transport company. You can buy a license for 5 years, so after these 5 years you need to renew the partnership contract. Otherwise your license will be revoked. This means that the value of this invisible asset is equal to 0. This decrease in the value of this intangible asset is known as amortization.

5. Earning

Revenue-generating assets are company assets that are ready to operate and generate profits. On the other hand, there are also non-productive assets. For example, your company keeps assets in the form of gold in case of urgent need. Therefore, this gold is a non-productive asset.

Type of Liability

1. passive editing

Fixed liabilities are a type of debt whose value does not change easily over a year. An example is a long-term debt principal. prepaid income, etc.

2. Current Passive

The opposite of fixed liabilities is current liabilities. which is a type of debt whose value can easily change within 1 year, such as short-term debt, part of long-term debt that must be repaid within 1 year, etc.

Difference Between Assets and Liabilities

Assets and liabilities are two important things. financial statements company. However, there are significant differences between these two, namely:

1. Understanding

Assets are resources that are available to the company for future business operations and profits. While liabilities are liabilities owed by the company to third parties. Either as an owner, investor or lender.

2. Input method

Assets and liabilities are entered in different formats. In a general journal, if it increases, the asset information is entered in the Debit column, and if it decreases, the asset information is entered in the Credit column. On the other hand, the increasing liability must be entered in Credit. while if it decreases then it is entered in the debit column. So, Total assets and liabilities must be balanced..

Examples of Assets and Liabilities

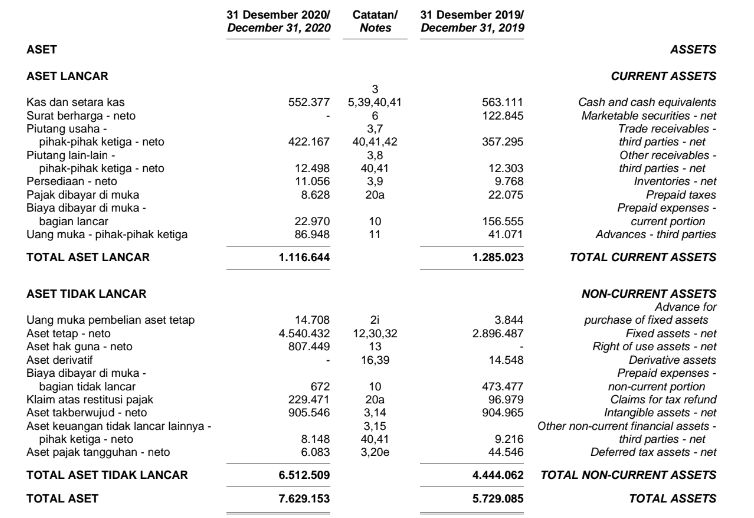

To better understand the difference between assets and liabilities. Please see the financial position report of PT Centratama Telekomuniks Indonesia Tbk below:

From the above three numbers In conclusion, although the totals between 2019 and 2020 are different, the total assets and liabilities (liabilities + equity) of companies with stock code CENT are the same, i.e. Rp 5.72 and Rp 7.6 trillion respectively. .

for personal money management Knowing the difference between assets and liabilities can help you develop a better financial plan. For example, you have IDR 5,000,000 in debt that needs immediate repayment and don’t have that much cash or savings.

Once you know the components of your property and list your property. It turns out that you still have a used gaming laptop (device) that is no longer being used and that you can sell to pay off debt. In this way, you can pay off your debts without further hassle.

[ad_2]

Source link

{kind=link}